We’ve all seen the big headlines over the few past few years proclaiming various new oil fields. These stories often go on to claim how the Age of Oilquarius is now upon us and we will swim and bathe in seas of energy until the sun explodes and the universe ends. We are often showered with numbers and statistics that upon closer inspection don’t mean anything useful at all.

Case in point is the announcement earlier this year that a large oil field had been discovered in the Australian outback. Check out these three headlines and bylines below:

Trillions of dollars worth of oil found in Australian outbackUp to 233 billion barrels of oil has been discovered in the Australian outback that could be worth trillions of dollars, in a find that could turn the region into a new Saudi Arabia.$20 trillion shale oil find surrounding Coober Pedy 'can fuel Australia'

Oil discovery in Australia’s outback could ‘transform world’s oil industry’

Pretty heady stuff. The first headline goes straight for the Benjamins, mentioning an undefined ‘trillions of dollars’ and then follows up with the astronomical number of 233 billion barrels. It ends with the George Clooney of the oil world, the country that everyone wants to be, Saudi Arabia. Where do I sign up?

The second headline also carries the money line and adds that holy grail in energy circles of ‘ENERGY INDEPENDENCE.’ The headline asks us to dream of the Australian oil utopia where true blue Ozzies no longer have to buy oil from those troublesome Arabs. Neither does anyone else because Australia is now a net oil exporter! Hooray! Unfortunately they also mention that pesky detail that Coober Pedy has somewhere between 3.5 billion and 233 billion barrels of oil. One of those numbers is quite a bit bigger than the other one (we will revisit this later).

Finally we have the slightly more sober ‘transform world’s oil industry’ which isn’t really that much more sober when you consider that the revenue for Conoco Phillips is larger than the GDP of Pakistan, the revenue for Chevron is larger than the GDP of the Czech Republic and the revenue for Exxon Mobil is larger than the GDP of Thailand, i.e when we we talk about transforming the world’s oil industry we are talking about some major world changing activities.

So I hear you ask: why are these headlines so fantastic? The first reason is just one word. Hype.

1. Hype

Hype is what marketers do to sell people things they don’t really want or need. The above headlines are the news story equivalent of a store proclaiming ‘up to 70% off selected items.’ Never mind that once your in the store you find you don’t actually want any of those luckily selected 70% off items: half the battle is already won. You are already in the shop and that greatly increases the likelihood of you buying something else .

Like stores, oil companies want people to buy their product. Although in the case of oil exploration companies initially the product they are selling is an investment with the potential to have a large pay off down the line. Of course the larger they can hype the market the more people will be interested and more likely to invest. A few might be turned off by deeper reading into the flaky numbers but there are more than enough people out there with wads of cash who are willing to take a gamble. Hence the company attracts investors and the board of directors live sweet for a couple of years on the investment capital until the next big find.

2. Most people don’t understand basic mathematics

The second reason why oil companies get away with overblown estimates is because most people don’t understand basic mathematics.

Taking the example above the Coober Pedy could hold somewhere between 3.5 billion and 233 billion barrels. Most people don’t stop and think about how huge the difference in those numbers actually is. If we converted that to a salary of $3,500 and compared it to $233,000 we see very easily how the former wouldn’t last more than a few months while latter would provide a wealth of excess. Another way of thinking about it is that 233 billion is over 6550 percent larger than 3.5 billion.

Scientifically the confidence intervals would be so wide as to be absolutely meaningless. But most people don’t get this and so oil companies continue to pedal this hogwash.

3. The bystander effect

It’s basic human nature to avoid a problem until it starts affecting you personally. It is also basic human nature to avoid a problem if everyone else is also avoiding the problem. The is called the bystander effect or Genovese syndrome. For example an accident with a crowd standing around: because the majority of bystanders are doing nothing about it, the less likely it is for anyone individual to break the mold and help those involved in the accident. This is occurs because as the number of bystanders increases an individual is less likely to notice the situation, interpret it as a problem and less likely to assume responsibility for taking action.

In the realm of energy activism there are only a small number of people willing to risk their careers and reputations in calling for an end to the status quo. The majority of people don’t even notice our addiction to oil let alone see it as a problem. Therefore the oil companies throw around any numbers they like and barely anyone not already interested in energy takes any notice.

4. Keeping business as usual

Given that we live in an age of sound bites and miniscule attention spans what we read in the form of headlines is incredibly powerful. This creates problems when those headlines aren’t entirely truthful and we can’t even have a frank and open discussion about our energy future because “everything’s fine, they keep finding big ones everywhere.”

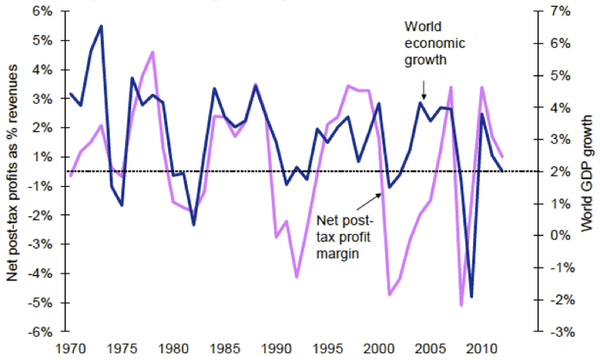

If we look at the figures above comparing oil company profits to countries GDP’s we can see that oil companies are doing pretty darn well for themselves. They don’t want anything to change that could threaten their profit margin. They have a vested interest in keeping business as usual.

There is a concerted effort to downplay the occurrence of peak oil and to reinforce that there is plenty of affordable oil left in the world. Because if people really start getting spooked en mass then governments could be forced into seriously looking into alternative energy, the last thing any oil company really wants.

By reporting overblown field estimates oil companies keep people passive and unconcerned about their future. This means oil companies can get on with making as much money as they possibly can while cheap oil is still relatively accessible.

5. Warding off effective action on climate change

There is a wealth of evidence that oil companies have invested huge amounts of money in disinformation campaigns to confuse the public about climate change. By downplaying climate change and continuing to attract investment with overblown field estimates oil companies can continue with the most environmentally damaging industry on earth.

Overblown field estimates keep investors away from alternative energy projects and keep governments away from effective climate change policy as they vie for petro dollars.

In these tough financial times governments are jumping over each other to look attractive towards oil companies. Oil companies promise huge financial benefits for the relaxation of pesky environmental laws and the increase in penalties for protesting against oil companies.

So next time you see an article proclaiming a huge amount of oil or gas in an area, stop for a second and think about how those companies might be benefitting from such positive press. Because more than likely the truth might be buried a little more deeply than the provocative headline.

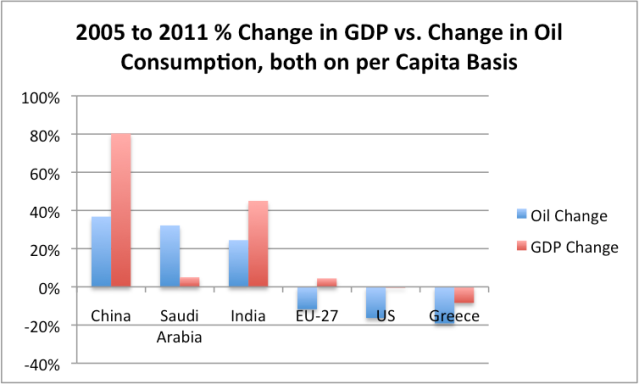

Figure 2: Comparison of 2005 to 2011 percent change in real GDP vs percent change in daily oil consumption, both on a per capita basis. (GDP per capita on a PPP basis from World Bank, oil consumption from BP’s 2012 Statistical Review of World Energy, NZ population data from Statistics New Zealand.)

Figure 2: Comparison of 2005 to 2011 percent change in real GDP vs percent change in daily oil consumption, both on a per capita basis. (GDP per capita on a PPP basis from World Bank, oil consumption from BP’s 2012 Statistical Review of World Energy, NZ population data from Statistics New Zealand.)